Demand for money and its types. Nominal and real demand for money

The aggregate (total) demand for money (Dm) includes:

1) business demand - demand for money to pay for goods and services,

2) demand for money as a reserve value (store of value).

Business demand, demand for transactions – Dm 1. Each economic entity at any given moment must have a certain amount of money (cash balances) in order to be able to carry out transactions without hindrance. Households need money to buy goods, pay utilities, etc. Businesses need money to pay for raw materials, materials, payments, etc.

The amount of demand for “cash balances” depends on nominal GNP, i.e. business demand for money is directly proportional to the real volume of GNP and the price level. Obviously, an increase in real GNP leads (all other things being equal) to an increase in income, which stimulates more spending and a greater demand for money for transactions. The same direct relationship exists between business demand and prices. It is known that the purchasing power of money is measured by the number of goods and services that can be bought with it. If prices rise, the purchasing power of money falls, and more money will be needed to keep real incomes the same.

Thus:

Dm 1= f (Q,p) > 0,

where Q is the real volume of gross national product;

p – absolute price level.

People save part of their income, and these savings can be made either in cash (accumulation of cash or funds in deposit accounts) or in the form of various financial assets (government securities, stocks, bonds, etc.). Each of these forms of savings has its own benefits. Money is absolutely liquid, but does not generate income. Securities are less liquid, but generate income. Hence: the demand for money as a store of value or the demand for money from assets - Dm 2 - depends on preference.

If economic entities prefer to have highly liquid assets, the demand for money increases, if less liquid, but profitable, it decreases. In turn, the question of how savings are distributed between money and non-monetary assets is decided depending on the interest rate.

If the interest rate rises, then the exchange rate (price) of securities falls, their profitability increases, and economic entities prefer to save in the form of non-monetary assets - the demand for money as a store of value falls. And vice versa.

Dm 2 = f (i) > 0,

where i is the interest rate level.

Thus, money depends on the real volume of production, the price level and the rate of interest.

Connecting the money supply (Sm) with the general demand for money (Dm) gives a picture of the money market. The money market is a market in which the demand for money and its supply determine the level of interest rates, the “price” of money.

The main participants in the money market are: firms, government, central and. The object of purchase and sale is money provided for temporary use. The peculiarity of the money market is that, unlike commodity markets, where the process of purchase and sale represents the exchange of goods and services at prices measured in monetary units, in the money market money is actually exchanged for other liquid assets at opportunity cost, measured in nominal units interest rates.

Since it is not determined by their price, but is regulated by the state, based on the general goals of macroeconomic development, the supply of money is completely inelastic.

Equilibrium means the equality of the amount of assets that economic agents want to have in the form of money and the amount of money that is offered. This equilibrium is achieved at a certain interest rate.

If the interest rate exceeds the equilibrium level, then economic agents will not want to have the amount of money offered by the banking system. As the interest rate has risen, the value of securities has fallen, they have become more profitable, and economic agents will prefer non-monetary assets to monetary ones. A fall in the demand for money will lower the interest rate to the equilibrium level.

When, on the contrary, the interest rate turns out to be less than the equilibrium rate, the number of people willing to hold their assets in securities decreases. Those with savings will increasingly favor liquidity, recognizing that low interest rates equate to high security prices. Demand for securities will fall, which will cause their prices to rise. An increase in the price of securities will reduce the demand for them and increase the demand for money. This will be reflected in interest rates, which will go up towards equilibrium.

As in any market, the equilibrium achieved in the money market can be disrupted by various non-price factors.

1. Changes in GNP affect the amount of real income, and, therefore, affect business demand and the demand for money as a store of value. A change in demand under the influence of a change in income will lead to shifts in the demand curve for money and (all other things being equal) to a change in equilibrium.

2. When presenting a demand for money, economic agents take into account its purchasing power, which is measured by the number of goods that can be bought with it. When the prices of goods rise, the demand for money increases. This circumstance is a decisive factor for understanding inflation. An increase in demand for money can serve as a signal for an increase in money supply, which initiates a further rise in prices.

3. A change in the supply of money, a shift in the supply curve, also leads to a change in the interest rate, which, in turn, affects investment demand, output and employment.

Thus, we can draw an important conclusion: the money and commodity markets are closely related. Events occurring in the money market are reflected in the commodity market. In turn, changes in the volume of production of goods and services are reflected in the demand for money, and fluctuations in interest rates affect investment and aggregate demand.

The demand for money is the need for a certain amount of money. It is determined by how much material assets firms and the population want to keep in checks and cash.

The demand for money is a natural phenomenon in the market. Two approaches can be considered to explain it:

Classical (monetarist);

Keynesian.

The classical approach determines the demand for money supply from the position of the equation: RU=MB, while M is money in circulation, B is the speed at which money circulates, P is the price index, Y is the size of the issue. It must be taken into account that speed is a constant value. When considering the situation over a long period, of course, B may change. For example, if new technologies appear in the banking sector.

From the above equation we can conclude that it depends on the dynamics of changes in GDP or RU. If this value increases by 3% over the year, then the demand for money will increase by the same amount. This means that the funds are quite stable.

As in any market, along with the needs, there are those who are ready to satisfy them. The money supply is quite unstable and depends on government decisions. But in accordance with the classical theory, or Y, on the contrary, changes slowly. Factors of production play a significant role here, which are usually quite stable in the short term. Therefore, it is better to consider changes in the money supply within one year or more. This indicator has a significant impact on the price level and has virtually no effect on employment. This phenomenon in economics is called monetary neutrality. The monetarist rule states that the state should strive to maintain the growth rate of the supply of money at the level of GDP. Then their supply will correspond to demand, and prices in the economy will be stable.

The quantity theory explains two motives for money demand. The first is that companies and people need cash as a tool for servicing transactions. The purchase of goods or services occurs mostly by exchanging them for bills and coins. Less often, the buyer and seller use barter (services) for another product (service). The need for funds for purchases is called the demand for money for transactions. Let's consider several factors influencing it:

The volume of goods currently on the market;

Price level for services and goods;

National income.

But the greatest influence is exerted by the level of income: M = Ufact. Here M is the demand for money, Ufact. - national income.

The second motive for money demand is associated with precautionary purchases. It arises due to the fact that people often have to deal with payments that they could not foresee before. Therefore, they should always have at least a small reserve of cash. Money demand, according to the above formula, is directly proportional to national income.

Both motives of money demand do not depend on the interest rate. On the graph, the demand line looks like a straight line located vertically.

J. Keynes identified a third motive for storing money - speculative. It implies that if savings are kept at home, then the owner misses out on possible profits. That is, the money could be invested in less but more profitable ones. The demand formula looks like: M = Ifact. Here is Ifakt. - interest rate level. The relationship between these indicators is directly proportional. In graphical form, the speculative demand line is a curve with a negative slope.

Control over the money supply in the country is exercised by the Central Bank. This is necessary so that the money is at a stable level.

General demand for money.

The total demand for money is the sum of the demand for money for transactions and the demand for money from assets. The overall demand for money depends on the value of the gross national product and the interest rate. The money supply can be changed with the help of certain measures on the part of the government. The government must control the money supply, that is, the issue of both cash and credit, and manage the money supply to achieve certain goals. Let's take a closer look at the consequences of a change in the money supply and a change in the interest rate. In the money market, where supply and demand collide, demand is a relatively stable and predetermined value of the gross national product (in terms of the demand for money for transactions) and the interest rate (in terms of the demand for money from assets ). And the money supply can be changed by pursuing certain policies on the part of the government and the Central Bank. Changing the money supply has certain consequences. Let’s assume that a temporary equilibrium has been established in the money market at the moment; people have as much money in their hands as corresponds to their demand (desire), predetermined by the factors described above. We can say that as much money was put into circulation as corresponded to demand. Now imagine that the supply of money has increased. “If people were satisfied with the size of their money holdings, and the total money supply increased, then over time people will find that they have accumulated too much money and will try to reduce their actual money holdings to the desired level.” (Heine). They will change their cash reserves by changing the structure of their assets - for example, by buying shares of corporations or government bonds. An increase in the money supply will increase the demand for all other types of assets - financial assets and goods. This will lead to an increase in prices for goods, an increase in prices for bonds, shares and a decrease in the market interest rate for the use of money. The structure of assets will change until the marginal profitability of all types is the same.

If there is less money in circulation than the demand for it (the desire to have money in reserve), then people will again try to change the structure of assets. They will try to reduce their purchases, which will lead to lower prices for goods. They will also sell real estate, stocks, bonds, which will lead to a decrease in their market prices. This process will continue until the marginal benefit of all assets is the same. In this case, the interest rate for using money will increase. Thus, by influencing the quantity of money supply, it is possible to influence many processes, since changes in the volume of money supply affect the state of the economy as a whole.

Equilibrium in the money market. Monetary aggregates.

Money is in constant movement. The cash form of money circulation is the movement of cash, i.e. coins and banknotes. Coins are an ingot of metal of a special shape and standard, banknotes are bank notes issued by the central bank of the country. The non-cash form of money circulation is associated with non-cash payments.

Monetary circulation is subject to a certain law, which determines the amount of money necessary to ensure commodity circulation in the country.

D + (R - K + P - V) / O,

Where D is the amount of money;

P - the sum of prices of goods to be sold, rubles;

K - sum of prices of goods sold on credit, rubles;

P - the sum of prices of goods for which the payment period has already arrived, rubles;

B - the amount of mutually extinguishing payments, rubles;

O is the speed of money turnover in a given period of time.

The equation of exchange is a calculated relationship according to which the product of the money supply and the rate of turnover of money is equal to the product of the price level and the real value of the gross national product

M CH O = R CH N,

Where M is the amount of money in circulation;

O - speed of money turnover per year, rub.;

P - price level of goods, rubles;

N is the real value of GNP, rubles;

R CH N - nominal value of the gross national product, rub.

The equation of exchange shows a relationship that leads to the fact that the amount of money in circulation will correspond to the real need for it. The state must support this relationship by pursuing the correct monetary and financial policies.

Currently, monetary aggregates are used to analyze changes in the process of money movement. Monetary aggregates - these are types of money that differ from each other in their degree of liquidity.

M about - cash in circulation;

M 1 = M o + funds of legal entities in settlement and current accounts + demand deposits of individuals in commercial banks;

M 2 = M 1 + time deposits of individuals and legal entities in commercial banks;

M 3 = M 2 certificates of commercial banks + bonds of freely negotiable loans, etc.

In order for monetary circulation not to be disturbed, monetary aggregates must be in a certain equilibrium.

Using monetary aggregates, you can determine the speed of money turnover:

O = N/M 2,

Where O is the speed of money turnover, turnover;

N is the annual volume of GNP, rubles;

M 2 - monetary aggregate, r.

3.6.5. Demand and supply of money. Equilibrium in the money market

The money market is the relationship between the supply and demand of money, where the “price of money” is the interest rate. The demand for money is the amount of means of payment that economic entities wish to hold at the moment.

Demand for money stems from two functions of money - as a means of circulation and the unity of preserving wealth. In the first case we are talking about demand for money for making deals purchases and sales (transactional demand), in the second - on the demand for money as a means of acquiring other financial assets(primarily bonds and stocks). Transactional demand is explained by the need to store money in the form of cash or funds in checking accounts and other financial institutions in order to make planned and unplanned purchases and payments. Demand for money for transactions is determined mainly by the total monetary income of society and changes in direct proportion to the nominal value of GNP. Demand for money to purchase other financial assets determined by the desire to receive income in the form of dividends or interest and varies inversely with the level of interest rates. This dependence is reflected by the money demand curve D m.

The total demand curve for money D m denotes the total amount of money that the population and firms want to have for transactions to purchase stocks and bonds at each possible interest rate.

Theoretical models of money demand

Demand for money and quantity theory. The modern interpretation of quantity theory is based on the concept of the velocity of money in the movement of income, which is defined as:

where V is the velocity of money circulation, P is the absolute price level,

Y is the real volume of production, M is the amount of money in circulation.

If we transform the formula for this level: M=P*Y/V, we will see that the amount of money in circulation is equal to the ratio of nominal income to the velocity of money circulation. If we replace M on the left side of the equation with the parameter D m - the amount of demand for money, we get:

From this equation it follows that the quantity demanded for money depends on the following factors:

Absolute price level. All other things being equal, the higher the price level, the higher the demand for money and vice versa;

The level of real production volume. As it grows, real incomes of the population increase, which means that people will need more money, since the presence of higher real incomes also implies an increase in the volume of transactions;

Velocity of money circulation. Accordingly, all factors influencing the velocity of money circulation will also affect the demand for money.

Demand for money in the Keynesian model. J.M. Keynes considered money as one of the types of wealth and believed that the part of assets that the population and firms want to store in the form of money depends on how highly they value the property of liquidity. M-1 money is a liquid asset. Keynes called his theory of money demand liquidity preference theory.

As J. Keynes believed, three reasons encourage people to keep part of their wealth in the form of money:

The use of money as a means of payment (transactional motive for storing money);

Ensuring in the future the opportunity to dispose of a certain part of one’s resources in the form of cash (precautionary motive);

The speculative motive is the holding of money, arising from the desire to avoid capital losses caused by holding assets in the form of bonds during periods of expected increase in interest rates.

It is this motive that forms the feedback between the amount of money demand and the interest rate.

Modern theory of demand for money. The modern theory of demand for money differs from the theoretical model of John Keynes in the following features. She:

Considers a wider range of assets beyond interest-free cash holdings and long-term bonds. Investors can hold portfolios of both interest-bearing forms of money and non-interest-bearing forms of money. In addition, they must have other types of liquid assets: funds in savings and time accounts, short-term securities, bonds and shares of a corporation, etc.;

Rejects the division of the demand for money on the basis of transactional, speculative and precautionary motives. The interest rate affects the demand for money, but only because the interest rate represents the opportunity cost of holding money;

Considers wealth as the main factor in the demand for money;

It also includes other conditions that influence the desire of the population and firms to prefer a liquid asset, for example, a change in expectations, with a pessimistic forecast for the future environment, the demand for money will increase, with an optimistic forecast, the demand for money will fall;

Takes into account the presence of inflation and clearly distinguishes between such concepts as real and nominal income, real and nominal interest rates, real and nominal values of the money supply.

The money demand function uses the nominal interest rate. I. Fisher describes the relationship between nominal and real interest rates with the following equation:

where i is the nominal interest rate; r – real interest rate; P is the inflation rate.

According to the quantity theory, an increase in the money supply increases inflation, and inflation increases the nominal rate. This dependence is called the Fisher effect.

Money supply is the totality of means of payment circulating in a country at a given moment. It includes cash outside the banking system (C) and deposits (D): M S =C+D.

The amount of money depends on the size of the monetary base, i.e. assets of the central bank, the norm of minimum reserve coverage, the amount of excess reserve of commercial banks and the share of cash in the total amount of means of payment of the population.

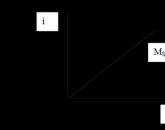

Graphically, the supply curve looks like this:

The higher the interest rate, the greater the supply of money for a given monetary base and a fixed reserve coverage rate. With an increase (decrease) in the monetary base, the money supply curve will shift to the left (right); with a decrease (increase) in the reserve coverage rate, the supply curve will shift to the right (left).

The volume of money supply is determined by the behavior of the population, the Central Bank and commercial banks.

Money market- this is a market in which the demand for money and its supply determine the level of interest rates, the “prices” of money; it is a network of institutions that ensure the interaction of demand and supply of money.

In the money market, money is not “sold” or “bought” like other goods. This is the specificity of the money market. In money market transactions, money is exchanged for other liquid assets at opportunity cost, measured in units of the nominal interest rate.

The condition in the money market when the amount of money supplied is equal to the volume of population demand for money is called money market equilibrium. If the money supply in a society is controlled by the Central Bank, and prices and economic goods are stable, then the money supply curve will have a vertical appearance. E is the equilibrium point.

The demand for money is a decreasing function of the interest rate. If it increases, then the demand for money increases (curve D L) shifts to the right and the interest rate increases. A reduction in the money supply will have a similar effect.

A decrease in the lending rate occurs when income and demand for money decrease, as well as when supply increases.

| Previous |

Demand for money(demand for money) is a general concept used in economic analysis to explain the desire of economic entities to have at their disposal a certain amount of means of payment, or the general market need for money.

The demand for money is determined by two functions of money - to be (that is, money necessary for concluding transactions); to be (that is, money is needed to accumulate and acquire new assets). There are various theoretical models of the demand for money - within which they analyze the different reasons that give rise to it.

Thus, J.M. Keynes (1883-1946) identified three motives that generate the demand for money:

- transactional (transactions motive) - the need for money as;

- precautionary motive - saving money in case of unplanned expenses;

- speculative motive - the demand for money to preserve wealth in the face of uncertainty about future interest rates.

Demand for money to make transactions- the amount of money that people want to have for use as a medium of exchange for making payments. The demand for money for transactions changes in direct connection with changes in the nominal value.

Demand for money as an asset- the amount of money that people want to keep as savings. The demand for money as an asset changes inversely. When interest rates are low or the opportunity cost of holding money is low, people choose to hold more assets in the form of . When interest rates are high or opportunity costs are high, liquidity is too expensive and people hold fewer assets in the form of money.

Demand for money for speculative purposes- demand for cash balances that are stored in liquid form, for their possible use with benefit when the price of an asset decreases. The decision to hold cash balances depends on the interest rate. If the current interest rate is high, people prefer to hold assets in the form of , rather than in the form of , due to the high opportunity cost of holding money and the negligible risk of loss: interest rates are unlikely to rise further and cause bond prices to decline. In other words, there is an inverse relationship between bond prices and . Speculative transactions are the result of expected price changes. If interest rates are low and bond prices remain high, people will prefer liquidity due to low opportunity costs, expectations of a rise in interest rates, and a corresponding fall in bond prices. The result is an inverse relationship between the interest rate and the demand for speculative balances. The speculative demand for money, along with the demand for money for transactions and the demand for money for unforeseen purposes, forms aggregate demand for money.

Interest elastic demand for money, is the demand for money, sensitive to changes in the interest rate.

Demand for money is not interest elastic, is the demand for money, insensitive to changes in the interest rate.

The recognition of the existence of a stable demand for money formed the basis of the theory of monetarism. Based on this assumption, it can be shown that fiscal policy is neutral, i.e., when government spending pushes interest rates higher, private sector output falls accordingly. Moreover, changes in the money supply are a necessary and sufficient condition for changes in the nominal value of gross domestic product, or changes in . However, econometric studies have not been able to reliably establish whether the demand for money is actually stable.

The demand for money has different interpretations in different theories.

Monetarism views money in circulation as the main tool of macroeconomic analysis.

Within the framework of the quantity theory of money, the demand for money is determined in accordance with the equation (model) of N. Fisher:

M V = P QWhere M– the amount of money in circulation;

V– velocity of money circulation;

Q– number of goods sold;

R– average price of goods and services.

After transforming the equation:

MD = (P Q)/VWhere M.D.– the amount of money demanded.

If we assume that transactions are taken into account in , then P·Q equal to nominal GDP. From here M V = GNP and onwards

MD = GNP/VThe modern interpretation of the quantity theory of money by M. Friedman takes into account the demand for money of an individual, which is limited by the amount of his “resource portfolio” - money and other assets:

MD = P f (R b , R e , p, g, y, u)Where M.D.– the amount of demand for money;

R– absolute price level;

Rb– nominal interest rate on bonds;

R e– market value of income on shares;

R– rate of change in the price level in percent;

g– the relationship between human wealth (labor) and all other forms of wealth;

y– total amount of wealth;

u– a value reflecting possible changes in tastes and preferences.

Modern monetarism has rival theories of money - Keynesianism and neo-Keynesianism. Keynesian theory attempts to determine the demand for money based on the economic entity's motives for storing part of its wealth in the form of liquid monetary assets. J.M. Keynes, as noted above, identifies the following motives: transactional, speculative, precautionary. It is important that the subject cannot always determine exactly what motives he is guided by in his demand for money.

Transactional is the motive for storing money, based on the convenience of using it as a means of payment. Precaution is a motive for storing money in order to be able to make unplanned expenses in the future. Speculative is a motive for storing money, which arises from the uncertainty of future market value and the desire to avoid losses.

Keynes believed that the demand for money depends on nominal income and the rate of interest: nominal income has a direct proportional effect on money demand, and the rate of interest has an inverse proportion.

The main differences between monetarism and Keynesianism are as follows.

Unlike Keynesianism, which focuses on the regulatory role of the state, monetarists are closer to the old classical school and often reject government intervention in regulation.

Keynesians assign a secondary role to money; monetarists believe that it is money circulation that determines the level of production, employment and prices.

There are different positions in the interpretation of the velocity of circulation of the money supply. Monetarists believe that velocity (V) is stable. But if the velocity of circulation of money (V) is stable, then from the equation (M · V = P · Q and further M · V = GNP) it really follows that there is a direct and predictable relationship between the money supply M and GNP.

Keynesians believe that a change in the money supply first changes the level of the interest rate, then and only through it causes a change in nominal GNP.

Monetarists believe that in long-term policy the state must ensure a justified constant increase in the money supply (M).

Unlike monetarists, Keynesians believe that the build-up is fraught with many negative consequences. If the supply of money increases, then the demand for it falls, and the price of credit also decreases, i.e. interest rate, it ceases to respond to the growth of money supply. As a result, the economy falls into and breaks the chain of cause-and-effect relationships between the amount of money and nominal GNP. Therefore, unlike monetarists, Keynesians consider the main means of stabilizing the economy, and not.

Gradually, both of them abandon their extreme positions, so the contradictions between them are smoothed out and a Keynesian-neoclassical synthesis emerges in the field of monetary theory, which is currently becoming dominant among economists.

Popular

- Investment demand Keynesian concept of investment demand

- How to start investing money: Instructions and examples How to become a successful investor from scratch

- How to create a trading plan for a trader (example) How to create a Forex trading plan

- What time does forex open? What time does forex trading end on Friday?

- How to invest in the Chinese stock market

- Contextual advertising specialist - who is he and what does he do?

- Small business grants: where to find and how to get them

- Government assistance to small businesses

- Grants for beginning entrepreneurs Money from the state for starting a business

- Product promotion on Instagram: make yourself known to millions