The break-even threshold is calculated. How to calculate the break-even point: to help entrepreneurs

Every entrepreneur thinks about methods of earning money and ways to make a profit. In any production there are costs - expenses for the production and sale of goods. They will be deducted from the revenue received, the result of the calculations will be profit (positive value) or loss (negative value).

For profitable operation, the management of the enterprise must know the boundary value of the transition of loss to profit. This is called the break-even point. It is used by investors to determine the likelihood and payback period of projects.

The break-even point can be determined using mathematical calculations or graphically. The value will be in monetary or in-kind equivalent.

What's happened

The break-even point or critical volume is considered to be the quantity of products produced at which the income received from sales will cover the total costs. In other words, this is the amount of minimum profit in monetary terms or the number of products sold, which compensates for costs.

Work at this point indicates the absence of profit and costs at the same time. If the volume increases by at least 1 unit, the enterprise will begin to operate at a profit. The break-even point is often called the profitability threshold.

Purpose

The break-even point value is used to analyze the current financial condition and allows you to plan for the future. The indicator makes it possible to:

- assess financial stability and solvency, which is used by investors, management and creditors;

- calculate the feasibility of expanding and developing new types of products and technologies;

- see the dynamics of changes in the indicator, identify production bottlenecks;

- sales plan planning;

- establish an acceptable reduction in revenue that will allow you to remain profitable;

- trace the influence of production costs, cost of goods and volume sold on the financial result.

Calculation

The calculation can be made in various ways, depending on the type of costs. Let's consider the classical order, which underlies the remaining methods.

Data for calculation

To correctly determine the break-even point, you should distinguish between fixed and variable costs and know:

- unit cost of goods - R;

- produced and sold volume - Q;

- revenue received - IN(not required to determine the profitability threshold);

- the amount of fixed costs - Zpost.

- variable costs - Zper.

Fixed costs mean costs incurred that do not depend on the volume produced, that is, they remain unchanged for a long time. These include:

- wages with insurance contributions for management and engineering staff;

- rental of premises;

- tax payments;

- depreciation;

- leasing and loan obligations.

Variable costs will be costs that depend on the quantity of products produced. They have different meanings and respond quickly to changes in production. Variable costs are:

- price of raw materials, spare parts and components;

- piecework wages and insurance payments for production workers;

- HMS, electricity, fuel;

- transportation.

Cost sharing is conditional and is used to determine the break-even point. The specifics of some enterprises imply a more detailed division according to economic meaning. For example, production costs are:

- conditionally permanent: storage and warehouse movement of components;

- conditionally variable: costs for current and planned repairs.

There are several cost accounting systems: variable costing, direct costing, standard costing, etc. Each type of cost can be individual for a certain type of product.

Formula

The mathematical method (MEP) allows you to determine break-even points in physical and monetary terms. The classic scheme involves calculation for one product. If it is necessary to determine an indicator for several types of products, then averaged data is used in the calculation. The following assumptions apply:

- Each type of cost and cost of goods remains constant for the selected volume.

- Directly proportional change in output and cost.

- Production capacity in the period selected for calculation is constant.

- Unchanged product range.

- Insignificant influence of inventories - the share of work in progress is small, and all products are released for sale.

BEP is often confused with the payback period of a project. This is the time after which the organization will receive a profit from the investment.

Definition in monetary terms

Using the calculation, you can find out the minimum value of revenue that will help cover the costs of production and sales. Profit will be 0.

VERDEN = V*Zpost/MD

MD = V-Zper

B = P*Q

IN- revenue;

P- cost of production;

Q- volume produced;

MD- marginal income, which can be calculated per unit of production, taking into account that revenue will be equal to the product of price and volume.

MD for 1 unit. = P - Zper. for 1 unit

The break-even point in monetary terms is found through the marginal income coefficient - Kmd:

Kdm = MD/V =MD per 1 unit/R

VERDEN = Zpost/Kmd

The final value when calculated using the two formulas must be the same.

Definition in kind

The above formula allows you to determine the minimum volume of products sold that can cover production costs and lead to zero profit.

VERNAT = Zpost/(R-Zper by 1 unit)

Each subsequent unit that allows you to exceed a certain volume will bring profit to the organization. If the break-even point in physical terms is known, then it is easy to calculate the break-even point in monetary terms:

VERDEN = VERNAT * P

Graphical method

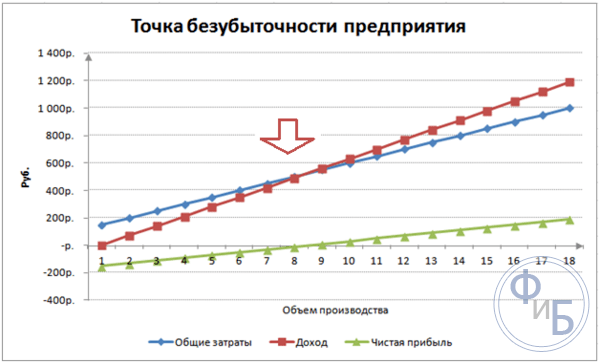

The graphical method allows you to determine the break-even point without mathematical calculations. They build a graph showing revenue, fixed and variable costs. The horizontal axis will be volume, and the vertical axis will be the amount of costs and revenue in rubles.

The break-even point will be at the intersection of total costs and revenue. On the chart, this value is equal to 91.67 pieces with revenue of 22,916.67 rubles.

Calculation in Excel

For ease of calculation, you can use the Excel office application. It is easy to establish connections between data and build tables with graphs for comparison.

Compiling a table

It is necessary to begin calculating the break-even point by entering data on costs and cost of goods. For example, fixed costs are 150 rubles, variable costs are 50 rubles, and the cost of a unit of goods is 70 rubles.

Based on the entered data and production volume, a table is generated where the dynamics of changes in net profit or loss should be traced. This is necessary to determine the break-even point.

Let's create a second table with columns:

- Volume of production.

- Fixed costs.

- Variable costs.

- Total costs.

- Revenue.

- Marginal income.

- Net profit.

The volume of production is chosen independently. In the example, 0-20 pieces are taken. Fixed costs are transferred from the first table in cell D3. Since fixed costs do not depend on the volume of products produced, their value remains unchanged throughout the entire column. To save the value of a cell when propagating values, place a $ - $D$3 sign in front of the address.

Variable costs are determined by the formula:

Zper = Q*Zper for 1 unit. = A9*$D$4

Total costs, also called gross, are equal to the sum of variable and fixed costs - B9+C9.

Revenue or income is equal to the product of volume times the cost of a unit of goods - А9*$D$5, and marginal income is E9-C9.

Net profit, as mentioned above, is equal to marginal income minus fixed costs: E9-C9-B9.

From the eighth unit the organization will begin to make a profit. With a smaller volume, revenue cannot cover total costs. The first profit is 10 rubles, that is, this is not exactly the break-even point when total costs are equal to revenue. The exact value can be determined by the formula:

TBnat = 150/(70-50) = 7.5 pcs.

The mathematical value of the break-even point is 7.5, but it is not possible to produce any part of the whole product. Economists round the value up - 8 pcs. The proceeds will be 560 rubles.

You can add two additional indicators to the table - margin of safety (margin of safety) in monetary and percentage terms (KB%, KBden). This will help determine how much revenue is missing before reaching the break-even point and how much total costs need to be reduced to reach the break-even point at a certain volume. Using these ratios, you can determine a safe financial situation - when it reaches 30%.

KBden = Vfact - Vtb = E9-$E$14

KB% = KBden*100%/Vfact = H10/E10*100

VTB- revenue for the security point;

In fact- actual revenue.

Plotting a graph

For understanding, make a graph. There are several types of charts in Excel. The best way to perceive the information in this example is the scatter plot, which is located in the “Insert” tab. The horizontal axis is the volume of products produced, and the vertical axis is revenue and the amount of costs. Data for construction:

- total costs;

- net profit;

- revenue.

There are three straight lines on the graph. The intersection of total costs and revenue will be at the breakeven point. It shows zero net profit horizontally and minimum revenue to cover incurred costs vertically.

To build a detailed graph with contribution margin and variable costs, you need to expand the amount of data.

Calculation example

The simplest calculations are for mono-production, when an organization produces the same type of product. Multi-product problems have their own characteristics that should be taken into account when calculating the break-even point.

One product

Let's consider a common example of entrepreneurial earnings - trading on the market. The product is watermelons with a fixed price throughout the city. Watermelons are bought in the southern regions and brought to the central part of the country. The business is seasonal, but quite profitable.

Basic indicators:

- the cost of 1 watermelon is 250 rubles;

- Zper for 1 unit. (salesperson salary, wholesale purchase) - 130 rubles;

- Postage (taxes, market space rental, transportation, packaging) - 11,000 rubles. per month;

- monthly revenue - 36,000 rubles.

For successful planning, it is necessary to calculate the minimum sales volume and the profit value to cover the costs incurred.

The indicated cost is averaged, since the weight of each watermelon is different. These values can be neglected in the calculation.

Determining the break-even point:

VERNAT = 11000/(250-130) = 92 pcs.

To determine in monetary terms, calculate the volume of watermelons sold and the value of variable costs for this volume:

Q months = 36000/250 = 144 units;

Volume limit = 130*144 = 18,720 rubles.

Let's determine the profitability threshold in money using various formulas:

VERDEN = 3600*11000/(36000-18720) = 22916.67 rubles

VER den = Zpost/((250-130)/250) = 22916.67 rubles

VERDEN = 92*250 = 23,000 rubles

The first and second values show the break-even point when the profit is 0. In this case, the sales volume is 91.67 watermelons, which is incorrect information. The third indicator is based on a critical volume of 92 watermelons.

When compared, it is clear that monthly revenue exceeds the break-even point, which allows us to talk about profit.

Safety edge:

KBden = 36000-23000 = 13000 rubles;

KB% = 13000/36000 * 100% = 36.11%

The level is more than 30%, which indicates the correctness of business planning.

Multiproduct task

Let's consider the calculation procedure for a store that sells four goods: A, B, C and D. The store incurs fixed costs and has variable costs for each type separately. Purchases are made from different suppliers, and sales revenue is also different.

Initial data:

- A: revenue 370 thousand rubles, variable costs 160 thousand rubles;

- B: revenue 310 thousand rubles, variable costs 140 thousand rubles;

- B: revenue 340 thousand rubles, variable costs 115 thousand rubles;

- D: revenue 70 thousand rubles, variable costs 40 thousand rubles.

The total revenue is 990 thousand rubles, and variable costs are 455 thousand rubles.

The revenue structure remains constant. Due to the fact that the range and cost of goods vary, it is better to calculate the break-even point in monetary terms. The decision will be based on the direct costing method, which assumes a range of values:

VERDEN = Zpost/(1-Kz.per.);

Kz.per. - share of variable costs in revenue:

Kz.per. = Zper/V

- A - 0.43;

- B - 0.45;

- B - 0.48;

- G - 0.57;

- General Kz.trans. - 0.46.

Let's determine the marginal income and its share in revenue:

- A - 210 thousand rubles, 0.37;

- B - 170 thousand rubles, 0.55;

- B - 125 thousand rubles, 0.52;

- G - 30 thousand rubles, 0.43;

- The total value is 535 thousand rubles, 0.54.

Let's calculate the average break-even point:

VERDEN.sr. = 400/(1-0.46) = 740.74 thousand rubles.

Next, we will consider the most optimistic forecast - marginal ordering in descending order. The highest profitability will be for the first two products A and B. Initially, the store should sell these products, which will provide a marginal income of 210 + 170 = 380 thousand rubles. This will almost cover the fixed costs of 400 thousand rubles. The remainder can be taken from the third item. The break-even point will be reached after the sale of the listed goods:

VERDEN. optim. = 370+310+(20*240/125) = 718.4 thousand rubles.

A pessimistic forecast or marginal ordering in ascending order would be the sale of G, C, B. The total marginal income is equal to 325 thousand rubles, which will not cover fixed costs. The remaining 75 thousand rubles must be received from the sale of product A. The value of the break-even point:

VERDEN. pessim. = 70+240+310+(75*370/210) = 752.14 thousand rubles.

As you can see, the break-even point is different in the three cases. Optimistic and pessimistic values give the range of possible break-even points.

Let's determine the safety margin in percentages and rubles:

KBden =990-740.74 = 249.26 thousand rubles;

KB% = 249.26/990*100% = 25.18%.

Despite the profit, the store's safety margin is less than 30%. It is necessary to take measures to improve financial performance. To do this, you will need to reduce the Zper and increase the volumes for goods A, B and D. It would not be superfluous to conduct a detailed check of fixed costs in order to find reserves for their reduction.

Calculation for the enterprise

Let's consider an organization that produces household solvent, which is sold in liter containers. The enterprise is small, the cost rarely changes, which allows you to calculate the break-even point in physical terms.

Data for calculation:

- the cost of one bottle is 140 rubles;

- variable costs per 1 liter - 80 rubles;

- fixed costs - 170 thousand rubles;

- revenue - 450 thousand rubles;

- volume - 3 thousand rubles.

VERNAT. = 170,000/(140-80) = 2833.33 pcs.

The calculated value is close to the actual volume - 3000 pcs.

Let's define the safety edge:

KBnat. = 3000 - 2834 = 166 pcs.

KB% = 166/3000 * 100% = 5.53%

It can be concluded that the company is on the verge of breakeven. Urgent measures should be taken to improve the situation: reconsider the cost structure; the remuneration of management personnel is probably too high. They study variable costs in detail and find cheaper suppliers.

Advantages and disadvantages of calculations

The main advantage of calculating the break-even point allows you to quickly and easily analyze the level of production or sales that is necessary to achieve the minimum critical level. The disadvantage of the above model is its construction limitations:

- Linear change in sales and production. This does not allow us to take into account sudden surges and changes that occur in reality. Linearity does not take into account seasonality, decrease or increase in demand, or the entry of new competitors into the market. This all affects future demand, and accordingly sales volumes. New technologies can be introduced into production, which increases output volumes.

- The model is highly effective in a low-competitive market with stable consumer demand for manufactured products. Globalization is becoming the culprit of stability in the market.

- Sales volume depends on many factors: marketing, size of the dealer network, product quality, seasonality, etc.

- Such calculations do not show an adequate picture for small enterprises whose sales patterns are unstable.

Break-even planning

The listed methods are easy to calculate for one product and are suitable for companies with a stable market and a constant sales price.

However, there are a number of disadvantages:

- it is impossible to take into account seasonality and cost fluctuations;

- In markets, specificity often increases, progressive technologies and marketing moves appear;

- the cost of raw materials may vary;

- Regular customers and wholesalers are given discounts, which is not taken into account in the formula.

Analysis of the break-even point should occur in conjunction with various factors and economic indicators.

Based on the data obtained, the current market conditions and significant factors influencing the cost are analyzed. Planning is about forecasting costs and competitive value. The data is necessary for the break-even plan and production size, which are entered into the organization’s financial plan. For effective functioning, it is necessary to periodically monitor the implementation of approved goals.

Planning stages:

- Analysis of the current situation. It is necessary to identify strengths and weaknesses, as well as ways to reduce costs while taking into account external and internal factors. An assessment is made of sales and distribution services, the level of rationality of the production process and management. Among external factors, they must consider the market share occupied, the work of competitors, controlled companies, the economic and political situation, and changes in consumer demand.

- Forecasting future costs based on previously discussed factors. Alternative sales options are being explored, a competitive markup range is being planned, and the possibility of restructuring into production of similar products is being considered in the event of an unfavorable situation.

- Calculation of cost, fixed and variable costs. The size of work in progress, the need for working capital and fixed assets, and the sources of acquisition of working capital are determined. The costs should take into account possible expenses for leasing, credit and similar obligations.

- Calculation of break-even point. The required size of the safety edge is calculated: the less stable the external environment, the larger the safety edge should be. Then the release volume is determined taking into account the safety edge.

- Cost planning. The price of a product is calculated that will help achieve the desired level of sales. With the new cost, the break-even point, the safety margin, is re-determined. If necessary, points 3 and 4 are repeated to search for reserves for reducing cost and achieving the required safety margin.

- Approval of the final sales plan and break-even by period. Approval is made based on the value of the critical volume.

- Break-even control. It occurs in several stages: control of expense items, sales plan, cost, transfer of payment from customers. The management of the organization should always know the level of compliance of the current situation with the planned break-even value.

Calculating the break-even point helps determine the minimum production or sales limit for organizations. The model is well used in large production with a stable sales market. The break-even point model allows you to find a safe zone - the company’s distance from the critical value when profit becomes zero.

O.V. Grishchenko

Management Accounting

Lecture notes. Taganrog: TTI SFU, 2007.

6. USE OF ACCOUNTING INFORMATION IN THE PROCESS OF MAKING MANAGEMENT DECISIONS

6.2. One-component break-even analysis

Break-even analysis is a fairly simple in form and deep in content tool for planning and making management decisions in a commercial organization. The basis for making decisions regarding production activities is to consider options for possible changes in the market situation. Since the enterprise plan is a system of indicator values that the enterprise intends to achieve in the future, its implementation will depend on many factors. In the process of drawing up plans, the management of the enterprise will have to solve the following tasks:

– determine the volume of production that will not only cover costs, but also allow you to obtain the desired level of profit;

– determine the level of costs that allows you to remain competitive in the market.

Break-even analysis allows you to solve these problems. There are other names for this procedure in the literature, for example: “critical sales volume method”, “dead point method”, “zero profit point method”, “operational analysis”, “margin method”, cost-volume-profit method ", or CVP analysis (Cost - Volume - Profit).

The essence of the method is to determine for each specific situation the volume of output that ensures break-even activity.

One-component break-even analysis.

The simplest is the break-even analysis of single-product production, i.e. production that produces only one type of product. In general, without taking into account tax effects, the operating profit of an enterprise (P) for the reporting period is formed as follows:

P = VR – Zpost – Zper;

where BP is the enterprise’s revenue for the period in monetary units, BP = q × Q;

ts – selling price per unit of production, rub.;

Q – sales volume in physical terms, pcs, kg, etc.;

Zpost – fixed costs, rub.;

Zper – total variable costs, rub.

If we denote specific variable costs in rubles. – zper, then the formula can be presented in the following form:

P = (c – zper) × Q – Zper.

Break even(Qcr)– this is an indicator characterizing the volume of product sales at which the enterprise’s revenue from the sale of products (works, services) allows it to cover all expenses and reach a zero profit level (P = 0). The break-even point can be found from the equation:

Another important value that characterizes the cost structure of an enterprise is the value marginal incomeor contribution enterprises. Marginal income at manufacturing enterprises is considered to be the difference between the enterprise's revenue from the sale of products (works, services) and the variable costs that the enterprise incurred in the process of producing these products (works, services). There are different amounts of total marginal income (MI):

MD= BP – Zper = c × Q – zper × Q = (c – zper) × Q

and specific marginal income ( md):

md= c – zper.

There is another way to determine the amount of marginal income. The amount of marginal income can be determined by adding the fixed costs and profit of the enterprise:

MD = Zpost. + P.

The dependence model of the indicators under consideration can be constructed graphically (Fig. 6.2).

Rice. 6.2. Break-even chart

A widely used and very clear representation of profit growth above the break-even point is shown in Fig. 7.3. In this graph, straight line 3 complete is the x-axis. The ordinate axis reflects the amount of “divergence” between straight lines "Revenue" And Zfull, i.e. the amount of profit. When the output is below Qcr, the value on the ordinate axis will be negative (which corresponds to losses), and above Qcr - positive (profit). The slope of this graph to the x-axis will be equal to specific marginal income, and its intersection with the ordinate axis is the value Zfast, which is understandable - with zero output, losses are equal to the amount of fixed costs.

Rice. 6.3. Dependence of profit on output volume

The volume of production Qкр corresponds to the amount of revenue ВРкр, which, by analogy with output, is also called break-even point, in monetary units only:

![]()

or else:

,

,

Where UMD– share of marginal income in price.

The conclusion follows from the second formula: the higher the share of variable costs in the sales price of the product (ratio zper / c), the higher the break-even point. Otherwise, the lower the share of marginal income in revenue, the more products the company should produce in order to cover fixed costs and start making a profit.

Another indicator is calculated within the framework of break-even analysis - safety threshold(otherwise called marginal safety margin).This indicator is calculated asthe difference between actual volume and break-even point andindicates how much output can be reduced before the enterprise begins to incur losses. As already noted, the larger the output, the higher the profit. The higher the production volume, the less frightening an enterprise is from fluctuations in market conditions - the more fluctuations in costs and revenue it can safely endure, remaining in the “profit zone.”

Obviously, each specific volume of output has its own volume of security.

Let's look at the break-even analysis technique using an example.

Example.

The Zarya production enterprise produces dumplings. To develop a work plan for the next quarter, a break-even analysis of this single-product production is carried out. Planned variable costs for finished products of the enterprise are 3 per = 39 rubles. Fixed expenses for the quarter will be Z post = 480,000 rub. The selling price of dumplings is planned at the level of c = 67.5 rubles. Break even

![]() .

.

This volume of production will allow you to cover all costs and reach zero profit. If production for the quarter does not reach, the financial result of the enterprise will be negative, and the activity will be unprofitable.

Based on the level of annual profitability desired by the owners of the enterprise, the following level of target profit has been set - 100,000 rubles. Let's calculate what volume of output will allow us to get such a profit.

Having studied the market situation and the capabilities of their own enterprise, Zarya management planned the production volume of Q dumplings for the next quarter - . With this volume of production, the profit level will be:

P = (c – zper) × Qcr – Zper. = (67.5 – 39) × 20,000 – 480,000 = 90,000 rub.

Break even

Safety threshold:

The company's flexible budget provides for the possibility of an unfavorable situation in the planning period, which may lead to an increase in rent and, accordingly, fixed costs by 40,000 rubles. Managers of the organization do not consider it possible to increase the selling price of dumplings, since it is determined by the market. The simplest way to maintain the estimated level of profit is to cut variable costs. What savings in variable costs (s*per) will allow you to cope with an unfavorable situation?

Consequently, the company should achieve savings in variable costs in the amount of (39 – 37) = 2 rubles. on products. However, technologists and employees of the supply department, having studied all the possibilities for saving variable costs, came to the conclusion that it was impossible to achieve savings of more than 1.3 rubles. What fixed cost savings will this situation require?

Z*post = (c – z*per) × Qplan – P = (67.5 – 37.7) × 20,000 – 90,000 = 506,000 rub.

506,000 – 40,000 = 466,000 rubles.

480,000 – 466,000 = 14,000 rubles.

Thus, in order to compensate for a possible increase in rent, enterprise managers should, in addition to saving variable costs in the amount of 1.3 rubles. on products, it is necessary to find an opportunity to save 14,000 rubles in the existing structure of fixed costs.

Sales volume is the main indicator of a company's performance. It can be expressed in the actual number of units of products sold or in the total amount of funds received into the company’s account after the sale of goods. In economic analysis, gross, net, target and critical OP are calculated. The indicator is used when analyzing profits, costs, and break-even points. The source of information is financial reports, primary accounting documents, and management accounting data.

The central indicator reflecting the performance of any company is sales volume. It shows how many products, works and services the company created and sold. The profit and value of the business depend on the result obtained.

Volume of sales(Sales volume - SV, OP) is an indicator of the company’s operating results, which is represented by the total amount of revenue received over a certain period of sales of products, works, and services. It is often called the volume of product sales and is considered as a synonym for revenue.

Reference! Sales volume in financial analysis is expressed in monetary units (rubles, dollars, euros, etc.). However, for management accounting purposes, the possibility of using natural units (pieces, kg, m, etc.) is not excluded.

It is most convenient to consider the SV indicator as the actual amount of funds received into the company’s accounts during a certain period.

Break-even analysis

In the future, other indicators of economic analysis are calculated on its basis.

- If you subtract the cost of production from the OP, you can get a gross profit - a more accurate reflection of the efficiency of a business entity.

- If you compare the indicator with fixed and variable costs, you can calculate the break-even point.

Important point! When analyzing EP, it is impossible to compare it with the indicator of other companies or the industry average. It is compared with the results of the same company for previous periods or planned targets.

Sales volume reflects not only the company’s performance, but also the situation on the market: if demand for a product decreases, a high-quality substitute appears, or legal restrictions come into force, it will decline.

Sales volume: classification

In modern practice of economic analysis, several types of OP indicator are used:

- Gross - total sales for the reporting period at full prices without taking into account returns, discounts and other adjustments.

- Net - gross OP with the deduction of returns, benefits, discounts and other concessions to customers, which allows it to be used in assessing the efficiency of a company’s functioning and forecasting.

- Target - a planned indicator obtained by calculation based on information about the target profit.

Critical - the minimum amount of income that, even with unfavorable demand, allows the company to avoid losses.

Figure 1. Break-even point and critical sales volume

Formula for calculating sales volume

To determine the volume of product sales, it is not enough to use data from the company’s public financial statements: it will require the accumulation of information from primary accounting documents and internal management accounting documents.

The formula for estimating SV in general can be represented as an identity:

OP = (UPZ + EBIT) / (Tsed - Prev), where:

SPL - the sum of semi-fixed costs;

EBIT - profit before taxes;

Tsed - cost per unit of production;

Pre - variable costs for each unit of goods.

Reference! Semi-fixed costs are expenses that remain unchanged even if the volume of output varies. These include depreciation of buildings and structures, enterprise management costs, rental payments, etc. Variable costs, on the contrary, change along with an increase or decrease in the number of products produced.

The meaning of the indicator and its analysis

Since the OP formula takes into account costs and profit volume, this indicator is used in the analysis:

- Dynamics of actual sales volume.

- Changes in price levels.

- Volatility of production and distribution costs.

- Marginal income.

- Market demand, etc.

Important point! The total sales volume is an absolute indicator. It can be compared with the performance of competing firms when it comes to assessing market shares. In other cases, the dynamics of Sales volume are analyzed, as well as its proximity to the target value.

There is no general normative value for SV. Each company determines for itself a critical sales volume and target values, which become guidelines for changes in the indicator.

Reference! To determine the critical OP, the formula KOP = UPZ / (Tsed - Prev) is used, since the profit at the break-even point is zero.

The process of assessing the dynamics of a company's sales volume is presented in the video

Examples of coefficient calculation

In order to understand the practical application of the formula for calculating sales volume and analyzing this indicator, it is worth considering a ready-made example of calculating this indicator for the Kub company, which sells a standard model of DVRs.

Important point! If a company sells several types of products with different costs and prices, then SV is calculated separately for each type of product.

Conclusion! For three years, the OP of the Kub company has been decreasing. This negative trend occurs against the backdrop of rising EBIT and unit prices. Consequently, the reason for the reduction could only be a drop in the physical quantity of sold products.

It is worth noting that the critical output volume of the enterprise under study varies from year to year. However, it is lower than the obtained value and is 6.5, 6.1 and 6, respectively.

Conclusion! Until the actual SV value approaches the critical value, no action can be taken, but an unfavorable trend should be monitored.

A detailed scheme for calculating the volume of sales of goods, works, services and its critical value is given in a sample compiled on the basis of the tools of the Excel spreadsheet editor.

Questions and answers on the topic

No questions have been asked about the material yet, you have the opportunity to be the first to do so

Calculating the break-even point in Excel with examples

The break-even point reflects the volume of production, sales of goods and services, which covers all costs of the enterprise.

CVP analysis: calculation of marginal income and break-even point

In an economic sense, it is an indicator of a critical situation when profits and losses are zero. This indicator is expressed in quantitative or monetary units.

The lower the break-even point of production and sales volume, the higher the solvency and financial stability of the company.

Break-even point formula in Excel

There are 2 ways to calculate the break-even point in Excel:

- In monetary terms: (revenue * fixed costs) / (revenue - variable costs).

- In natural units: fixed costs / (price – average variable costs).

Attention! Variable costs are taken on a per unit basis (not total).

To find breakeven, you need to know:

Fixed costs (not dependent on the production process or sales) - rent payments, taxes, salaries for management personnel, leasing payments, etc.

Variable costs (depending on production volumes) - the cost of raw materials and materials, utility bills in production premises, workers' salaries, etc.

Selling price per unit of goods.

Let's enter the data into an Excel table:

- Find the volume of production at which the company will receive a net profit. Establish the relationship between these parameters.

- Calculate the volume of sales of goods at which the break-even point will occur.

To solve these problems, we compose the following table with formulas:

- Variable costs depend on the volume of products produced.

- Total costs are the sum of variable and fixed costs.

- Income is the product of production volume and product price.

- Contribution margin is total revenue minus variable costs.

- Net profit is income without fixed and variable production costs.

Let’s fill out the table and see at what output the enterprise will be “in the black.”

Starting from the 13th production, net profit became positive. And at the break-even point it equals zero. Production volume – 12 units of goods. And the income from sales is 120,000 rubles.

How to graph the break-even point in Excel

To clearly demonstrate the economic and financial condition of the enterprise, we will draw up a graph:

- We decide on the appearance of the graph and click the “Select data” button.

- For demonstration, we need the columns “Total Costs”, “Revenue”, “Net Profit”. These are the elements of the legend - “Rows”. We manually enter the “Row Name”. And in the “Values” line we make a link to the corresponding column with data.

- The range of horizontal axis labels is “Production Volume”.

We get a graph like:

Let's change the graph (chart layout) a little.

This demonstration allows us to see that the net profit at the break-even point is indeed “zero”. And it was after the twelfth release of the product that “plus” began.

Where are such calculations needed?

The “break-even point” indicator is in demand in economic practice to solve the following problems:

- Calculation of the optimal price for the product.

- Calculation of the amount of costs at which the company still remains competitive.

- Drawing up a product sales plan.

- Finding the volume of output at which profitability will appear.

- Analysis of the financial condition and solvency of the enterprise.

- Finding the minimum production volume.

Ready-made calculations and templates for analyzing an enterprise’s break-even point:

The results of such calculations are in demand by both internal and external users. Break-even is taken into account when making management decisions and gives an idea of the financial condition of the company. The use of such a model is a way to assess the critical level of production volume and sales of goods and services.

Online break-even point calculator

What is the break-even point and how to calculate it yourself

Let's look at the instructions for independently calculating the break-even point, with two test examples with formulas and graphs for retail trade and manufacturing activities.

The goal of any business is to make a profit. Every businessman has to predict the development of production, which is especially important when planning any new directions in it. Therefore, before the start of implementation, it is necessary to understand how effective the planned project will be, to assess the volume of investments, payback periods and financial risks. To carry out this assessment, there is an economic indicator - break-even point or, as it is also called break-evenpoint - BEP. Let's talk about this important economic tool, the need for its use and calculation methods.

Download two ready-made models for calculating the break-even point in Excel format for retail and industrial activities. In the examples given, you can change the source data to suit your numbers and calculate the BER directly for your project.

What does the break-even point mean, its importance in the functioning of the enterprise

The indicator determines the sales volume required to cover costs. Profit, which is the difference between revenue and expenses, is equal to zero. Those. The break-even point is the level of sales at which there is no profit and no loss.

It is calculated both in natural units and in value equivalent. This economic instrument determines the number of units of products, services or goods that need to be sold to cover costs and reach zero profit, as well as their cost. If the level of sales volume has not reached the calculated BEP indicator, it means that the company is incurring losses, and on the contrary, if it exceeds the sales volume, it means that the organization, having crossed the zero line, is making a profit.

What does the break-even point show?

- The BEP indicator determines such an important aspect of the company’s functioning as its financial stability. For example, an increase in the BEP value indicates objective or private problems in the company that led to a larger sales volume to achieve a zero profit threshold. The reasons for the growth of the indicator are the expansion and change in the structure of production, which invariably entails an increase in trade turnover, fluctuations in market prices, etc.

- The BER value allows a company to analyze the feasibility of investing in a new project, comparing the rate of self-sufficiency with the required sales volume, and its fluctuations - to establish the causes of problems in the company and their timely elimination, if they are not of a global nature.

- Calculating the break-even point of a project makes it possible to calculate optimal changes in sales volumes and product costs for more comfortable and flexible business. For example, calculate the non-critical value of the reduction in revenue in order to increase sales volumes, while operating at break-even and creating sufficient reserves.

Basic indicators for calculations

The calculation of BEP is based on information from production cost accounts. It is important here to divide them into constants and variables. Fixed expenses include expenses whose value does not change from month to month and does not respond to fluctuations in output and sales. It can be:

- depreciation of machines and equipment;

- salary of the AUP and social contributions accrued to it;

- rental, utility and other payments of an unchangeable nature.

Variable costs include:

- expenses for the purchase of raw materials and supplies for the product manufacturing process;

- payment for fuel and energy resources involved in the work process;

- wages of shop workers (with deductions), etc.

Fixed costs may change due to various reasons, for example, reduction/increase in production capacity, increase in energy tariffs, changes in rental payments, acquisition/disposal of equipment, inflation and other factors. The amount of variable costs fluctuates depending on the volume of output and sales.

Formulas for calculating break-even point

As already mentioned, calculations can be made in physical and monetary terms. Let's look at the basic data needed for calculations in units. Calculation data required:

- fixed costs for the full volume (Zpost);

- unit prices of a product or commodity (Tsed);

- variable costs per unit (Zper/unit).

Formula VER in units: BEPed= Zpost/(Tsed-Zper/unit) shows the sales volume in units to reach zero profit.

Calculating the value of BEP in monetary terms will require the use of the following data:

- fixed costs for the full volume (Zpost);

- revenue (B);

- product unit price (Tsed);

- variable costs for the full volume (Zper) and unit of goods (Zper/unit).

At the first stage of calculations, marginal income (Dm) is found, which is the difference between revenue and variable costs according to the formula: Dm= B - Zper.

Based on it, the coefficient (share) of marginal income in total revenue is calculated Kdm= Dm/V.

Using the coefficient, the value of BER is calculated in monetary terms: VERDEN = Zpost / Kdm

When forecasting new business directions, it is sometimes impossible to calculate the marginal income for the entire sales volume. In this case, the values of price and variable costs per unit of product or product are used, taking as a basis the formula

Dm/unit = C - Zper/unit, where Dm/unit is marginal income per unit.

When calculating the coefficient, this indicator is also used, comparing its value with the price of the product, because it is the revenue from the sale of a unit of goods:

Kdm= Dm/unit/Tsed, and get the coefficient value exactly the same as when calculating the entire sales volume.

So, the break-even point in value terms is calculated using the formula

VERDEN = Zpost / Kdm.

This indicator is also called the profitability threshold, which is very true, since by crossing this threshold - the amount that covers the invested costs, the company begins to make a profit.

Let's look at examples of calculating the break-even point for companies of different types of activities.

Example No. 1: calculating the break-even point for a retail enterprise

Let's calculate the profitability threshold for a women's clothing store. The assortment of a retail outlet is usually quite wide, so the practice of calculating in monetary terms is used here.

Fixed costs of a trading enterprise include costs associated with the work process:

- payment for rent of retail space, communication services, security, utilities, etc.;

- wages of sellers and contributions to extra-budgetary funds;

- advertising expenses.

Variable costs consist of sales volume and purchase price per unit of goods. Let's consider the presented table, which contains data for calculating the profitability threshold broken down into variable and fixed costs, calculated marginal income and its share in total revenue, and also calculated the required sales volume to reach a zero profit level.

Using the formulas, after calculating fixed and variable costs, we calculate:

- marginal income Dm = B - Zper. = 1,420,000 - 650,000 = 770,000 rubles

- margin coefficient Kdm = Dm / V = 770,000 / 1,420,000 = 0.542

- break-even point VERDEN = Zpost / Kdm = 155,000 / 0.542 = 285,844 rubles.

Conclusion: to cover the investment, sales in the amount of 285,844 rubles will have to be made, and sales of goods above this level will begin to make a profit.

Download break-even point calculation in excel for retail trade.

Features and methods of calculating the break-even point

The low complexity of the calculations in the previous example is due to the ideal conditions of the implied environment, which do not take into account the constantly changing market.

What is the break-even point and how to calculate it

The calculations of our examples allow for the persistence of such situations:

- the company does not change the price of products when sales volume increases;

- costs (both types) do not change. In reality, an increase in sales volume usually causes an increase in costs and expenses;

- the volume of production assumes full implementation, which is also rare in the process of activity.

Of course, this does not happen in life, but we provide an algorithm for the correct calculation, and the businessman himself has to adjust the calculations in accordance with the current market situation. There are different methods for calculating break-even point:

- mathematical (presented in example No. 1);

- graphic (more visual).

Both methods are very effective in calculating the indicator and are quite simple. Let's look at them using the following example.

Example No. 2: calculating the value of VER for a manufacturing enterprise

Industrial enterprises specializing in the production of products often produce a limited range of homogeneous products, for example, prefabricated parts of one unit. This method of planning production saves costs and greatly facilitates the calculation of the break-even point. For companies that produce a small number of items, it is easier to calculate the BEP indicator in natural values. Expanded production involves unification by product groups. In the presented example, there is a small enterprise that produces five types of products.

The calculation of the break-even point involves expenses grouped by variable and constant characteristics. We calculate the BER indicator in physical terms using the formula:

BEPed= Zpost/(Tsed-Zper/unit) = 281,400 / (674.71 - 332.35) = 930.7 units.

To calculate the indicator in monetary terms, you can use the following formula:

VERDEN = B * Zpost / (B - Zper) = 1,079,000 * 281,400 / (1,079,000 - 565,000) = 590,721.01 rub.

Conclusion: in order to reach a zero profit level, covering the invested costs, you should sell 930.7 units. products worth RUB 590,721.01. Subsequent sales will already be profitable and will begin to make a profit.

The graphical method for determining the value of VER is more visual. To do this, you need to build a graph by grouping the necessary data into a table.

The graph is constructed in the classical system, plotting data on production volume along the horizontal axis and revenue along the vertical axis. Using tabular information, they build revenue and cost lines.

The point of intersection of the line of received (or planned) revenue with the line of total costs is the break-even point. If you lower the perpendicular to the sales volume axis, you can find out the number of products required for sales in order to achieve a state of no losses and no profit. The value expression of this point is determined by drawing a perpendicular to the vertical axis. The graph clearly confirms the correctness of the mathematical calculations - 930.7 units should be sold. in the amount of RUB 580,721.01 to reach zero losses.

Downloadable model for a manufacturing plant.

If you have any clarifying questions about the calculation method or any difficulties using the formulas, ask them on the forum, we will help you figure it out.

Break even

Break even- the sales volume at which the company covers all its expenses without making a profit.

Its value plays an important role in the sustainability and solvency of the company. The degree to which sales volumes exceed the break-even point determines the margin of financial strength (margin of stability) of the enterprise. In turn, how profit grows with changes in revenue is shown by Operating Leverage (operating leverage).

Formula for calculating break-even point

To calculate the break-even point, you need to divide the costs into two components:

- Variable costs- increase in proportion to the increase in production (volume of sales of goods).

- Fixed costs- do not depend on the number of products produced (goods sold) and on whether the volume of transactions grows or falls.

Let us introduce the following notation:

| IN | — | sales revenue. |

| Rn | — | sales volume in physical terms. |

| Zper | — | variable costs. |

| Zpost | — | fixed costs. |

| C | — | price per piece |

| ZSper | — | average variable costs (per unit of production). |

| Tbd | — | break-even point in monetary terms. |

| Tbn | — | break-even point in physical terms. |

Formula for calculating the break-even point in monetary terms:

(in rubles, dollars, etc.)

Tbd = V*Zpost/(V - Zper)

Formula for calculating the break-even point in physical terms:

(in pieces, kilograms, meters, etc.)

Tbn = Zpost / (C - ZSper)

Example of calculating the break-even point

Look at the Excel spreadsheet

with a large assortment"

Calculation and graphs

The same data on the graph. Break-even point Tbn = 20 pieces

At the break-even point, the income line crosses and goes above the total cost line, the profit line crosses 0 - it moves from the loss zone to the profit zone.

How fixed costs, variable costs and price affect the break-even point, see Calculation of the break-even point, examples and graphs.

At first glance, the formula for calculating the break-even point is quite simple, and there should not be any difficulties in calculating it. But in reality, everything is not so simple.

Four important assumptions when calculating the break-even point

- We are talking about revenue (sales volume), so we believe that all for sale produced or purchased products. Warehouse stocks are not taken into account.

- Variable costs are directly proportional depend on sales volume. This doesn't always happen.

Procedure and rules for calculating the break-even point

For example, the case where in order to increase production volume it was necessary to build a new workshop will have to be calculated in a more complex way.

- Fixed costs do not depend from sales volume. This doesn't always happen either. If, in order to increase the volume of production, it was necessary to build a new workshop, hire more management personnel, increase payment for utilities - this case also does not fit the general formula.

- Break-even point is calculated for the enterprise as a whole or for some average product.

When calculating the break-even point, probably the most important limitation is assumption 4. To make the calculation for each product separately, you need to know what share of fixed costs falls on each product. If there are many products, calculating break-even points separately for each product becomes a complex task that requires a large amount of calculations.

Look at the Excel spreadsheet

“Break-even point and break-even analysis

with a large assortment"

Profitability, Min. markup, Marginal profit, Margin of safety

Calculation and graphs

Break even (break-even point) is the minimum volume of production and sale of goods (work, services), at which costs will be offset by income, and with the production and sale of each subsequent unit of production, the organization begins to make a profit. The break-even point can be determined in units of production, in monetary terms, or taking into account the expected profit margin.

The economic meaning of the break-even point The break-even point is the critical production volume. When the break-even point is reached, the profit and loss of the organization are zero. The break-even point is an important value in determining the financial position of an enterprise. The excess of production and sales volumes above the break-even point determines the financial stability of the enterprise.

The break-even model is based on a number of initial assumptions:

- the behavior of costs and revenues can be described by a linear function of one variable - output volume;

- variable costs and prices remain unchanged throughout the entire planning period;

- the product structure does not change during the planned period;

- the behavior of fixed and variable costs can be accurately measured;

- at the end of the analyzed period, the enterprise has no stocks of finished products left (or they are insignificant), i.e., the sales volume corresponds to the production volume.

Using the algebraic method, the point of zero profit ( break-even point formula) is calculated based on the following relationship:

I = S - V - F = (p * Q) - (v * Q) - F = 0

Where,

I is the amount of profit;

S - revenue;

V - total variable costs;

F - total fixed costs;

Q - production volume in physical terms;

v - variable costs per unit of production;

p - unit price (sales price).

From here we find the critical volume (break-even point in physical terms):

Q" = F / (p-v)

where Q" is the break-even point (critical volume) in physical terms.

The break-even point (the critical volume of production and sales of products or the profitability threshold) can be calculated not only in physical terms, but also in value terms:

Q" = Q" * p

Q” = F / [(p-v) / p]

Q” = (F*S) / (S-V)where Q” is the break-even point in value terms (the critical volume of production and sales of products).

The economic meaning of this indicator is revenue at which profit is zero. If the actual revenue of the enterprise is greater than the critical value, it makes a profit, otherwise - a loss.

The above formulas for calculating the critical volume of production and sales in physical and value terms are valid only when only one type of product is produced or when the output structure is fixed, i.e. the proportions between different types of products remain unchanged.

If several types of goods are produced with different marginal costs, then it is necessary to take into account the structure of production (sales) of these goods, as well as the share of fixed costs attributable to a specific type of product. The closure point of an enterprise is the volume of output at which it becomes economically ineffective, i.e. at which revenue is equal to fixed costs:

Qз = F/p

where Qз is the closing point.

If the actual volume of production and sales of products is less than Q", the enterprise does not justify its existence and should be closed. If the actual volume of production and sales of products is greater than Q", it should continue its activities, even if it receives a loss.

Another analytical indicator intended for risk assessment is the “safety edge”, i.e. the difference between the actual and critical volumes of production and sales (in physical terms):

Kb = Of - Q"

where Kb is the safety edge; Of - the actual volume of production and sales of products.

K = Kb / Qf * 100%

where K is the ratio of the safety edge to the actual volume.

The safety margin characterizes the risk of the enterprise: the smaller it is, the greater the risk that the actual volume of production and sales of products will not reach the critical level Q" and the enterprise will be in the loss zone.

Data on the value of marginal income and other derived indicators have become quite widespread for forecasting costs, sales prices of products, acceptable increases in the cost of production, assessing the effectiveness and feasibility of increasing production volume, in solving problems such as “make it yourself or buy it” and in other optimization calculations management decisions.

This is largely due to the comparative simplicity, clarity and accessibility of break-even point calculations. However, it must be borne in mind that the break-even model formulas are only suitable for those decisions that are made within an acceptable range of prices, costs and production and sales volumes. Outside this range, unit selling price and unit variable costs are no longer assumed to be constant, and any results obtained without such limitations may lead to incorrect conclusions.

Along with its undoubted advantages, the break-even model has certain disadvantages, which are associated, first of all, with the assumptions underlying it. When calculating the break-even point, they proceed from the principle of a linear increase in production and sales volumes without taking into account the possibility of a jump, for example, due to the seasonality of production and sales.

When determining the conditions for achieving break-even and constructing the corresponding schedules, it is important to correctly set data on the degree of utilization of production capacity.

Analysis of the break-even point is one of the important ways to solve many management problems, since when combined with other methods of analysis, its accuracy is quite sufficient to justify management decisions in real life.

Alexander Kaptsov

Reading time: 14 minutes

A A

Business activity of any scale involves making a profit. It is important for entrepreneurs to understand how long it will take for the company to reach the level of real income. Is this where the need to calculate the break-even point arises? What is this indicator? How to define it? What problems do entrepreneurs face when calculating and analyzing the break-even point, read the website

What does the break-even point show? Definition and meaning

In an economic sense, the break-even point is the income of a business organization at which the net profit indicator will be zero. In other words, the amount of revenue covers all expenses of the enterprise, both permanent and variable. Reaching the break-even point means recouping the total costs of the enterprise. Consequently, the company's further activities (and its subsequent implementation) will receive the status of profitable. As they say: the company will start working in profit.

What does a break-even indicator demonstrate to a businessman:

- What amount should be received into the company’s account? so that truly profitable activities can begin. What is the threshold for profitability in monetary terms? A conditional example, 100 rubles of income means zero work, and starting from 101 rubles, the company is in profit.

- What is the minimum sales volume . You can’t go lower, otherwise you won’t be able to recoup production.

- Indirectly indicates the minimum selling price . It becomes clear below what level there is no point in selling products.

The break-even indicator plays a major role in the planned investment. It reflects the effectiveness of the proposed project: payback time, degree of risk. Based on calculations, a business person can always determine whether this investment option is profitable for him or whether it is not worth participating in a risky venture.

What indicators are involved in calculating the break-even point?

When calculating the threshold beyond which real profit begins, it is necessary to determine the types of costs.

They are:

1.Permanent - independent of how much product is produced and how much of the finished product is sold. This expense may change with an increase/decrease in production capacity, a change in rent, during the depreciation of the ruble or inflation, or with a decrease (increase) in production space.

- Rent.

- Depreciation deductions.

- Salary of personnel from among administrators and managers (including deductions).

- Utility payments.

- Other expenses that do not change from month to month.

2. Variables – depending on the volume of products produced. Essentially, they increase as volumes of goods produced and, accordingly, sales increase. And in the same way, they decrease.

Among the variable (changing) expenses:

- The whole range of materials, components, workpieces.

- Fuel and energy costs used in the aspect of production needs.

- Workers' earnings with all deductions and so on.

Attention . If we consider the amount of changing expenses relative to one piece of product, then the production volume cannot influence this parameter. In this aspect, the value is conditionally constant.

Knowing the amount of expenses, the cost of goods sold, sales income and, of course, a special formula, it is easy to calculate the break-even threshold (profitability point).

How to determine the break-even point: determination methods and calculation formula

The value in question can be calculated using two formulas. The result of the first will be the natural value (product in pieces), the result of the second will be the value expression.

1. Formula for calculating the point of profitability (BER) in units of output:

BER = FC / (P - AVC), Where

F.C.– the amount of fixed costs.

R– price per piece of the finished product (service provided or work performed).

AVC– the amount of variable costs required for a unit of goods.

BER– naturally expressed permissible volume of sales.

2. Formula for calculating the break-even threshold (BER), expressed by the amount of money

In this case, it is necessary to start by calculating a special indicator that reflects income of a marginal nature, that is, showing what the share of margin is in the income received.

How is the contribution margin (MR) determined?

MR = TR – VC, Where

TR– revenue indicator.

V.C.– the amount of variable costs.

P=TR/Q

Q– is the sales volume.

Thus, the marginal return ratio (KMR) will be:

KMR = MR/P

The formula for calculating the break-even threshold (BER) looks like this:

BER = FC / KMR

Total ( BER) is equal to the amount of critical revenue. If it is less, losses begin.

Of course, illustrative examples will bring greater clarity to the understanding of the calculations of the point beyond which the company begins to work “in plus”.

How to calculate the break-even point for a manufacturing enterprise?

Enterprises typically engage in... Its price is approximately the same, which is not surprising, because this is a direct way to reduce costs. That is why in this case it is advisable to calculate the break-even threshold based on the natural expression.

For example, the cost of one manufactured product is 420 rubles.

The list of costs is given in the table:

| Name of fixed expenses | The name of the variable costs required to produce a unit of finished product | Unit cost, in rubles | |

| General plant type consumption | 82 000 | Materials | 155 |

| Depreciation type of deductions | 110 000 | Blanks | 92 |

| Salary of administrative and management staff | 110 000 | Workers' earnings | 65 |

| Communal payments | 25 000 | 22 | |

| Total | 327 000 | 334 |

Calculation of profitability point:

BER= 327,000 / (420-327) = 3,516 pieces

Consequently, the break-even of the enterprise is ensured by the production and sale of 3,516 pieces of finished products. If this volume is exceeded, the company makes a profit.

An example of calculating the break-even point in trading

Considering the specifics of the trade sector - the breadth of assortment and variety of prices - it is not advisable to calculate the break-even threshold in units of goods. Therefore, the result of calculations is always a monetary value. For clarity, let’s use the example of a children’s clothing store.

His expenses are in the table:

| Name of fixed expenses | Amount of fixed expenses, in rubles | Name of variable costs | Amount of variable costs, in rubles |

| Payment for rent of premises | 115 000 | Purchase price of one unit (average) | 1 100 |

| Salespersons' salaries | 135 000 | Planned sales volume | 650 units |

| The amount of deductions from accrued wages (approximately 30%) | 45 000 | ||

| Communal payments | 20 000 | ||

| Advertising expenses | 30 000 | ||

| Total | 345 000 | 715 000 |

This means that 345,000 rubles are constantly spent, the value of the handle is 2,800,000 rubles, with variable expenses of 715,000 rubles.

The amount of marginal income is equal to:

M.R.= 2,800,000 – 715,000 = 2,085,000 rubles

KMR = 2 085 000 / 2 800 000 = 0,75

Now you can start calculating the break-even threshold:

BER= 345,000 / 0.75 = 460,000 rubles

What does the calculation result say? To operate with zero profit, a store needs to sell clothes worth 460,000 rubles. Above this threshold, profitable trading begins.

The indicator of marginal income is interesting. It characterizes financial strength, or rather its reserve. In this version it is 2,085,000 rubles. It is by this figure that revenue reduction is allowed. A larger decline in revenue would drag the store into the unprofitable zone.

How to plot a break-even point?

Using the graphical method, a forecast is made of the company's main performance indicators under constant market conditions.

The graph shows the dependence of the goods sold on the proceeds and expenses:

- X axis reflects information related to sales volumes in units.

- Y axis demonstrates revenue and expenses in rubles.

When constructing a graph in the XY system, 4 lines are constructed:

- Direct fixed costs runs parallel to the Abscissa axis - they are unchanged.

- Variable cost line starts at the zero point and tends upward.

- Total expense line runs parallel to variable costs, but originates at a point on the Y axis, that is, its beginning corresponds to the beginning of fixed costs.

- Revenue line in the analyzed period assumes constant prices in a given period of time and uniform output.

Popular

- Business and Entrepreneurship

- Compare broker spreads

- Price Action Strategy: Definition of Patterns and Recommendations for Their Application

- Algorithms and stock trading: Hiding large trades and predicting stock prices Risks associated with algorithmic trading

- Labor market under conditions of perfect and imperfect competition

- Real biography of Dmitry Potapenko Who is Dmitry Potapenko really?

- What assets to invest in

- Pricing strategy of an educational institution

- We measure the Net Promoter Index (NPS)

- Forecasting demand, structure and sales volume